Application fraud is growing in residential rental markets since the COVID-19 crisis, according to a new analysis from Snappt, a real estate tech and fraud detection company. Applicant fraud has risen 9% month-over-month since the pandemic, with some inflating their income to qualify for rental or disguising the source of their income. Snappt researchers say that it’s likely a response to the economic climate as well as recent changes to local and state eviction moratoriums.

“There are a number of factors that are fueling the increase in fraudulent rental applications,” says Daniel Berlind, CEO and co-founder of Snappt. “The increasing number of self-employed applicants, a move to online rental applications, and the increasing availability of tools to fraudulently alter financial documentation all make the problem more common.”

Two thirds—or 66%—of property managers surveyed by Snappt say they’ve fallen victim to fraudulent rental applications. Here are the top five problems property managers are reporting from fraudulent lease applications:

Costs associated with having to evict bad tenants

Physical damage to the property

Missing out on renting to good tenants

Criminal activity at the property

Loss of reputation

It costs property managers an average of $7,685 per eviction, according to the report.

Borrowers with top-notch credit are scoring mortgage rates lower than the record average lows being reported. Freddie Mac announced the 30-year fixed-rate mortgage averaged 3.28% for the week ending May 14, but home shoppers with stellar credit could snag one with a rate of about 2.5%, according to The Mortgage Reports.

The Mortgage Reports’ daily rate survey shows that rates for 30-year, fixed rates for FHA and VA loans have fallen to 2.75%, in some cases. Borrowers with high credit scores, little debt, solid equity, and who shop around tend to find the lowest deals, The Mortgage Reports notes.

United Wholesale Mortgage, a residential mortgage lender, announced a 2.5% “Conquest” loan program for the 30-year, fixed- rate mortgage. “Some people said we’d never see interest rates drop below 3 percent on a 30-year mortgage,” says Mat Ishbia, United Wholesale Mortgage’s president and CEO. “We believe that the housing market is going to be strong, and we want to do our part to help more people get into their dream homes as we get through this pandemic together as a nation.”

Chase Bank followed suit by also offering mortgage rates below 3% on 30-year fixed-rate loans. Its offering for 30-year rates is as low as 2.875% (with a 2.944% APR).

Rates below 3% appear to be mostly reserved for purchase contracts and not refinancings, The Mortgage Reports notes. Refinance rates, for comparison, are falling in the 3.5% to 4% range.

Most Bay Area counties are easing restrictions, but at different degrees. It’s hard to keep track of what’s happening where. So we broke it down for you here. Scroll down to find updates for your county.

Santa Clara County will join other Bay Area counties in entering Phase 2 of the reopening plan. The new order will take effect Friday, May 22.

A core group of Bay Area counties released a joint statement Monday reporting significant progress on COVID-19 and its plan to being the early stages of Phase 2. The counties include Alameda, Contra Costa, Marin, San Mateo, San Francisco and Santa Clara.

The North Bay counties of Napa, Solano and Sonoma are already in Phase 2.

Alameda

May 18 – County officials released a list of business types currently authorized to operate here. You can also view the latest health order issued in the county, which provides further details on what restrictions are being eased as Alameda County moves into Phase. View it here.

May 14 – Health officials say based on the progress of their indicators and barring any big spikes in cases over the next few days, the county anticipates to safely move into “Early Stage 2” activities next week. This would include:

curbside retail and associated manufacturing and warehouses;

eligible businesses would align with state’s guidance where possible;

every organization and business should be working on plans that include physical distancing, training for employees on limiting spread of COVID-19, and disinfection protocols.

May 18 – County officials provided further details on the new health order beginning on Tuesday, May 19. Retail stores in the county may offer curbside sales or other outdoor pickups as long as they follow certain safety measures to prevent the spread of COVID-19. In addition, businesses that manufacture retail goods and provide warehouse or logistical support to retail stores to operate, but must limit the number of employees in inclosed areas so workers can comply with social distancing requirements.

May 15 – Officials announced a new order allowing outdoor gatherings during which participants stay in their vehicles and organizers follow revised rules. The new order takes effect May 19. Officials said it also gives new options for religious organizations who have been unable to hold services during the pandemic and for schools planning graduation ceremonies.

May 14 – Contra Costa County’s health officer said if the county continues to make progress and hospitalizations steadily decline, they will consider opening up all retail for curbside pickup plus all associated logistics and manufacturing next week. Officials did not have a timeline at this point.

May 14 – The county announced earlier this week it will move into Phase 2, which means retail will be reopening for curbside pickup. Manufacturing will also resume with restrictions. The county will also examine how “dine-in” will work.

May 14 – Retail will be allowed to reopen for curbside pickup and some manufacturing will resume with restrictions. Like other counties heading into Phase 2, Napa will have to figure out how “dine-in” will work in the county.

May 14 – San Mateo County Health Officer Dr. Scott Morrow plans to lift some restrictions, effective Monday, that would be consistent with early Phase 2 guidelines of Gov. Gavin Newsom’s Resilience Roadmap. That would effectively allow for retail businesses to operate from the curb and deliver. Manufacturing, logistics and some other businesses will be able to open with some modifications, county officials said.

May 14 – The city and county has announced it will allow retailers and manufacturers to enter Phase 2 of reopening. View our latest report here. And here’s a look at San Francisco’s guidance for businesses reopening on Monday. Check it here.

May 18 – Santa Clara County is joining other Bay Area counties in entering Phase 2 of the reopening plan as outlined by the state of California, according to a statement Monday from Supervisor Dave Cortese. A new health order announced by Santa Clara County Public Health Officer Dr. Sara Cody will go into effect May 22.

Under the new order, retailers are allowed to open for curbside and or outdoor pickup, and the supply chain for those retail establishments will also be allowed to reopen. The amended order allows additional outdoor activities to resume, including car parades, outdoor museums, historical sites, and public gardens.

May 14 – Solano County is already in Phase 2 under Gov. Newsom’s multi-phased plan to reopen the state. Retail is already open for curbside pickup or delivery, limited manufacturing is also open, and the county is finalizing its dine-in option plans.

May 14 – Sonoma County, like the other North Bay counties, is already in Phase 2. Retail is open for curbside pickup, limited manufacturing is open, and the county is examining what it will do for dine-in services.

The county announced it will be pushing even deeper into the second phase. Car washes and workers who can’t telecommute will be allowed to go back to the office. The county will also allow childcare for nonessential employees.

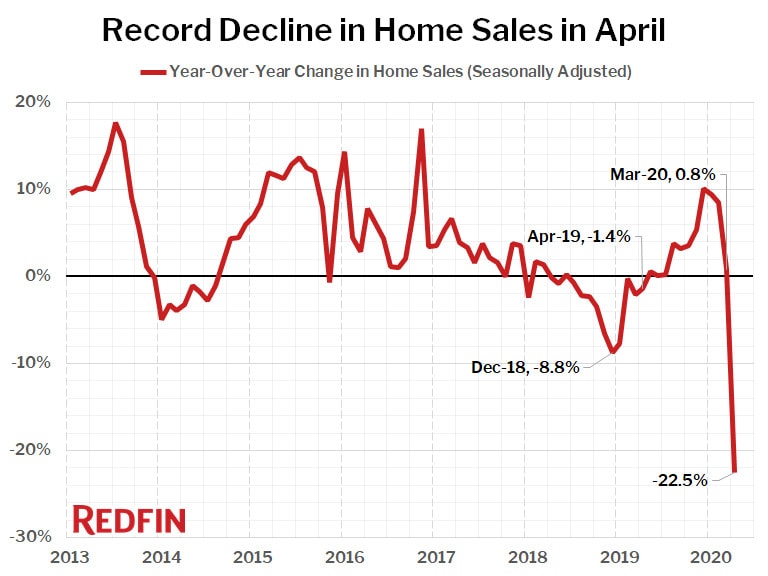

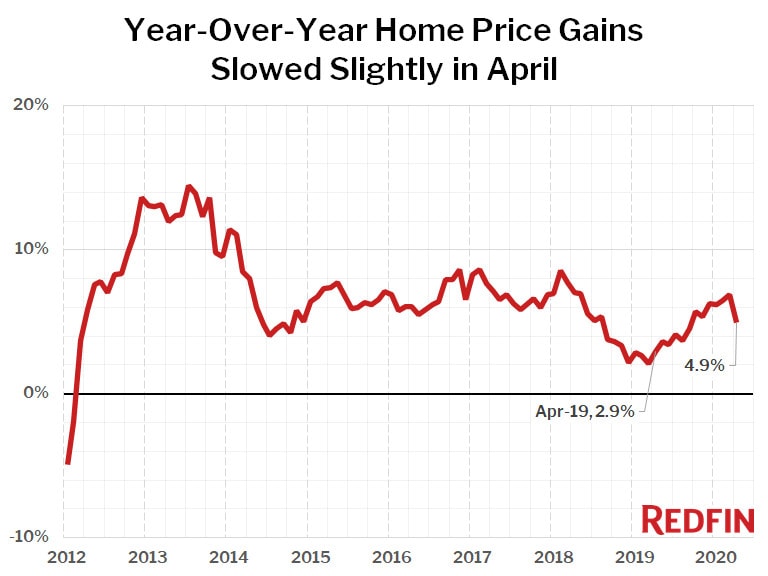

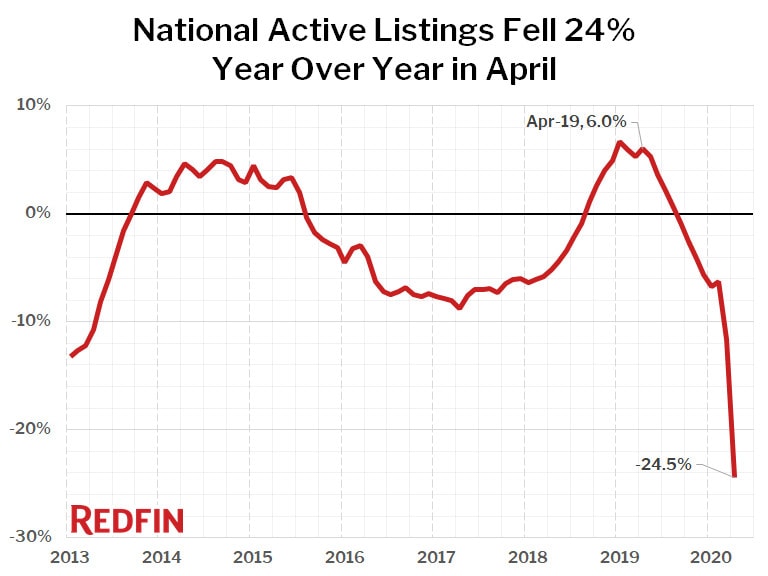

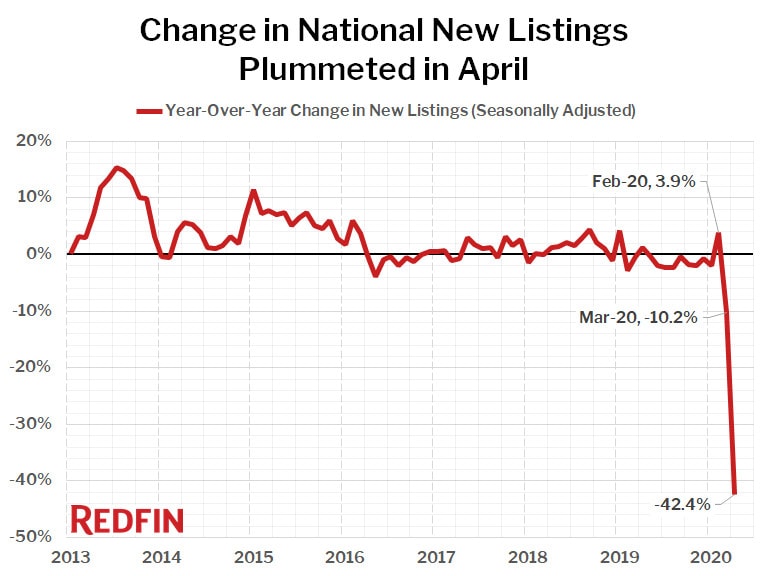

Supply of homes for sale was down 24% from a year ago in April and new listings fell by 42%, but home prices were still up 5%

The effects of the coronavirus pandemic and subsequent shutdowns hit the housing market in full force in April, with sales and listings both turning in historic declines from year-ago levels. In the past two months, the housing market has seen the fastest slowdown on record as it flipped from one of the strongest markets ever at the end of February to a near standstill in April.

Home sales in April plunged 22.5% from a year ago, as did both the number of homes newly listed for sale (-42.4%) and the number of homes available for sale (-24.5%). Home prices were still up from a year ago, but the rate of growth in the U.S. median home sale price stumbled slightly to 4.9% year over year, down from 6.9% in March. The national median sale price in April was $303,895.

April home sales fell 23% nationwide from March on a seasonally-adjusted basis, by far the largest decline on record (our data for this statistic goes back to January 2012). In general, markets with the biggest declines in home sales from a year ago were the most expensive, although due to especially tight restrictions on real estate during the shutdown, Detroit was also one of the three markets where sales slowed the most: San Francisco (-53.9%), Detroit (-46.8%) and New York (-45.8%).

Market Summary

April 2020

Month-Over-Month

Year-Over-Year

Median sale price

$303,900

0.3%

4.9%

Homes sold, seasonally-adjusted

409,100

-22.8%

-22.5%

New listings, seasonally-adjusted

361,800

-34.9%

-42.4%

All Homes for sale, seasonally-adjusted

1,662,200

-14.4%

-24.5%

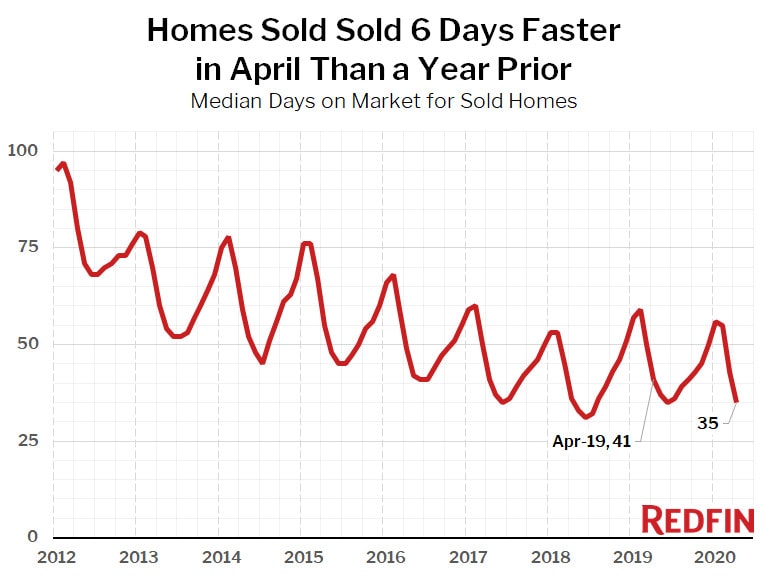

Median days on market

35

-9

-7

Months of supply

2.88

0.35

0.05

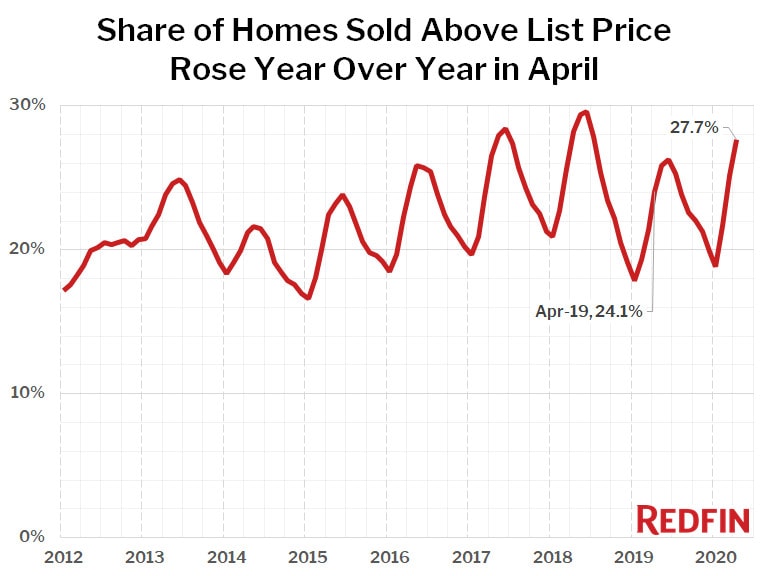

Sold above list

27.7%

2.5 pts†

3.6 pts†

Median Off-Market Redfin Estimate

$296,600

0.5%

1.7%

Average Sale-to-list

98.8%

0.2 pts†

0.4 pts†

† – “pts” = percentage point change

“The supply of homes for sale declined even more dramatically than homebuyer demand in April,” said Redfin lead economist Taylor Marr. “While home sales fell the most in more expensive markets, in more affordable areas prices continued to increase. Even during the depths of the slowdown last month the market was still faster and more competitive than it was a year earlier.”

Many of the nation’s most affordable housing markets are continuing to see sizable price gains. Nine of the top 10 metro areas where home prices rose the most year over year still had median prices below the national level, led in April by Detroit, (median price $159,900, +27.9%), Memphis ($217,000 +22.0%) and Philadelphia ($250,000, +19.0%).

Only one of the 85 largest metro areas Redfin tracks saw a year-over-year decline in the median sale price: San Francisco at -0.2%.

The national count of active listings of homes for sale fell 24.5% year over year during April, the biggest drop on record and the eighth straight month of declines. There were fewer homes for sale last month than any time since at least January 2012, which is as far back as we have recorded this measure. None of the 85 largest metros tracked by Redfin posted a year-over-year increase in the count of seasonally-adjusted active listings of homes for sale. The smallest declines were in Greenville, SC (-7.6%), El Paso (-8.0%) and Omaha (-10.2%). Active listings is a count of all homes that were for sale at any time during the month.

Compared to a year ago, the biggest declines in active housing supply in April were in Allentown, PA (-55.4%), Kansas City, MO (-48.8%) and Tulsa (-48.5%).

The number of new listings continued to plunge in April, falling 42.4% compared with a year earlier and down 34.9% from March. This dwarfs all other declines on record, although by the end of the month we did start to see listings begin to rebound.

So far the pandemic has only slightly slowed the rapid gains we had been seeing earlier in the year in the sales prices of homes. The median price of homes that sold in April was up 4.9% from a year earlier, slightly less than the previous four months, which all saw gains over 6%. However, even that dip was likely mostly caused by a decline in the number of high-end homes that are selling during this crisis relative to other price ranges.

“The typical time between when a home went under contract and when the sale closes is still about four weeks nationally,” explained Marr. “This means that many of the homes sold in April went under contract after the WHO declared that COVID-19 was a global pandemic, after initial claims for unemployment set new records, and after case numbers were already growing rapidly in the U.S. So, although some might have expected this dramatic disruption in the market to impact home prices, we haven’t yet seen evidence that it has had much of an effect.”

One thing that may be helping to prop up prices is low mortgage rates, which were as low as 3.29% during the first week of March when many offers were made on homes that sold in April. This was 1.12 percentage points lower than the same week of 2019, a monthly savings of $156 on the mortgage payment of the median-priced home.

Other measures of the market showed how competitive it was in April, despite lockdowns across the nation. Homes sold faster and a greater share sold for over list price than a year ago, clearly indicating that it is still a seller’s market.

Homes that sold in April spent six fewer days on market compared to the prior year. In April, the typical home went under contract in 35 days, compared to 41 days in April 2019.

The share of homes that sold above list price increased 3.6 percentage points year over year, coming in at 27.7% in April compared to 24.1% a year earlier.

Americans are resuming their house hunting online after taking a pause during the initial stages of the COVID-19 outbreak. One way to track potential buyer interest: internet searches.

LendingTree’s team analyzed Google search data to see how popular the search term “homes for sale” is in 50 of the nation’s largest metros. Overall, searches for the term “homes for sale” have risen in every metro tracked, compared to their 2020 lows at the onset of the coronavirus outbreak in the U.S..

By the end of April, the number of property searches had rebounded by 54%.

The metros with the largest percentage increase in Google searches for “homes for sale”: Tucson, Ariz. (up 164.71% by the end of April compared to its 2020 low); Rochester, N.Y. (up 118.92%); and Jacksonville, Fla. (up 96.08%).

From March to April, Tucson, New Orleans, and Miami posted the largest month-over-month increases in property search growth.

“There are probably people who think there are going to be bargains in the marketplace,” says Tendayi Kapfidze, LendingTree’s chief economist, about the property search rebound. “They might be anticipating that there will be fewer buyers competing because many people have had a disruption to their incomes or are uncertain about the outlook for their jobs. The low interest rates also make it an attractive time.”

Record low mortgage rates are sticking around. The week ending May 14 marks the sixth consecutive week that mortgage rates have stayed at or near all-time lows. The 30-year fixed-rate averaged 3.28% this week, Freddie Mac reports.

“Mortgage rates have stabilized at very low levels over the last few weeks as homebuyer demand slowly improves,” says Sam Khater, Freddie Mac’s chief economist. “Although purchase applications reached a new low in mid-April, purchase demand today is only down 10% from one year ago. While demand is improving, inventory is low and declining with no signs of a turnaround yet.”

Freddie Mac reports the following national averages with mortgage rates for the week ending May 14:

30-year fixed-rate mortgages:averaged 3.28%, with an average 0.7 point, rising from last week’s 3.26% average. Last year at this time, 30-year rates averaged 4.07%. The lowest average on records dating back to 1971 is 3.23%, which was set the week ending April 30.

15-year fixed-rate mortgages:averaged 2.72%, with an average 0.7 point, falling from last week’s 2.73% average. A year ago, 15-year rates averaged 3.53%.

5-year hybrid adjustable-rate mortgages:averaged 3.18%, with an average 0.3 point, rising slightly from last week’s 3.17% average. A year ago, 5-year ARMs averaged 3.66%.

Freddie Mac reports average commitment rates, along with average fees and points, to reflect the total upfront cost of obtaining a mortgage.

Acknowledging the many unknowns in relation to the COVID-19 virus, Lawrence Yun, chief economist for the National Association of REALTORS®, sounded cautious optimism about where the economy is heading and highlighted positive indicators in the residential real estate marketat the Residential Economic Issues and Trends Forum on May 13 at the 2020 REALTORS® Legislative Meetings. Yun predicted that steady and even rising home prices could point toward healthy home sales numbers once the economy reopens, and he saw signs that jobs could also rebound as stay-at-home orders ease.

Consumer Spending Down but Home and Garden a Bright Spot

Despite a decline in GDP, consumer spending, and business spending in the first quarter of 2020, Yun noted that residential investment, which includes home building, home sales, and remodeling, was actually up by 21% during the first three months—an indication, he said, of how strong the housing market was before the pandemic.

He also drew attention to the fact that personal income was up by 2% and personal savings jumped a remarkable 152%, related to curtailed household spending as the pandemic spread. Yun was hesitant to gauge the mindset of savers but offered more than one interpretation. “Are they waiting for the economy to reopen?” he said. “Or does it imply pessimism? There is certainly more money available.”

Noting that spending at grocery stores had predictably gone up in March while spending at restaurants had declined, Yun noted that restaurant spending had improved slightly in the last few weeks, showing a decline of just 60% to 70% from the same period last year as some restaurants found ways to continue serving customers by engaging in social distancing measures and offering takeout service.

And while clothing stores, sporting and hobby stores, and department stores all saw steep declines in consumer retail spending over the same period a year ago, building materials and gardening spending actually increased by 10.4%, a hopeful indicator. “People are upgrading their homes,” Yun said. “When the market reopens, that housing will go up in value. People are remodeling, working on lawn care. All things you do to sell a home.”

Jobs Rebound Possible in Education and Health

As grim as the unemployment numbers have been, Yun was encouraged by recent data. As of May 2, a reported 26 million people were jobless, in contrast to the high of 33 million who filed claims earlier in the lockdown. Yun inferred from the numbers that some people received unemployment checks for a few weeks and then got back to work, possibly in jobs in high-demand essential fields. He also said that it was important to watch for trends like these as a harbinger of improvement. “Even in good years people file (for unemployment),” he said. “We are looking for a flattening of the curve. When 1 million jobs are created in a week and less than 1 million file for unemployment, we will know the economy is turning for the better.”

Yun also noted that the biggest job losses in April were found in leisure and hospitality (7.6 million) and in education and health (2.5 million). However, he saw potential for the latter category to rebound quickly once the economy reopens. “I expect [education and health] to turn positive. People will need daycare. Hip replacement, knee surgery will be done again. These loses could be temporary.”

Home Prices and Sales

In addition to positive prognostications on the job front, Yun saw reason to be optimistic on the potential for home sales once the economy picks up steam. Of particular note were home prices, which he said were strong. “There is no meaningful downward trend,” he said. “If anything, they appear to be rising.”

Yun pointed to the current housing shortage as the source of the stable prices, and he predicted that the shortage could grow even more severe given that the usual spring increase in listings didn’t occur this year. He suggested that as the economy reopens, people will be ready to list. He noted that Georgia, which is beginning to reopen, could be a model for what we will see in the rest of the country as restrictions ease. “Listings are popping out,” Yun said, “and buyers are quickly grabbing homes.”

He added further that healthy home sales are possible even when the job market is uncertain. “Even in high unemployment times,” he said, “60 to 70 percent have employment. And we have record-low mortgage rates. The situation could be good.”

The pandemic doesn’t appear to be spooking some potential homebuyers away. Sporting masks and gloves, they’re rushing to preview homes in person, CNBC reports. But it’s home sellers who may be keeping them back.

“We’ve had buyers ready, willing, and able, and the sellers have been the ones who have pulled their homes, changed their minds,” Ben Hirsh, a real estate professional in Atlanta, told CNBC.

Indeed, new listings plunged nearly 40% annually during the week ending May 2, realtor.com®’s data shows.

For homes that are listed, buyers appear to be reemerging. A two-hour open house in Atlanta for a $3 million home this past weekend drew about a dozen families—mostly masked.

“It seems like the number of houses on the market had kind of paused,” one masked home buyer who attended the open house told CNBC.

Many buyers increased the online component of their home shopping using virtual tools when stay-at-home orders began in March. Real estate professionals stepped up offerings of 3D and virtual tours online as well as video walkthroughs in real time to interested buyers. Real estate professionals would visit the homes and walk around the house over a live video chat with an interested buyer.

But as states start to reopen, more homebuyers may be wanting to see those properties in-person.

Mike and Anna Elmers toured a home recently in Atlanta and told CNBC that after looking online at properties, they still wanted to get out in the field and see the homes for their own eyes. “We’re taking proper steps to wear masks and definitely social distance,” Anna Elmers says.

Record low mortgage rates last week may have offered up plenty of incentive for home buyers, even in a pandemic. Mortgage applications for home purchases increased 7% this week, which follows a 12% uptick last week, the Mortgage Bankers Association reports. Mortgage applications are viewed as a gauge for upcoming home sales.

This marks the third week in a row that purchase volume in mortgage applications has increased. The strongest growth in purchase applications was reported in Arizona, Texas, and California, the MBA reports.

The increase is occurring as half of the states in the U.S. have lifted some sheltering restrictions and have started to begin resuming more economic activity.

“Although purchase activity remains almost 19% below year-ago levels, this annualized deficit has decreased as more states reopen amidst the apparent, pent-up demand for home buying,” Mike Fratantoni, the MBA’s chief economist, says.

The MBA reported that the average contract rate on the 30-year fixed-rate mortgage fell to a record low of 3.4% last week.

But those low rates didn’t prompt a refinancing boom last week. The MBA’s index showed refinancing applications were down 2% last week compared to the previous week. The MBA says that many lenders lately are offering higher rates for refinances than for purchase loans.

Mortgage experts say that the decline in refinancing applications also may be due to the number of job losses from the pandemic that have restricted homeowners’ ability to apply for a new loan.

Real estate professionals report that about 77% of potential sellers are preparing to sell their homes once stay-at-home orders from the COVID-19 pandemic are lifted, according to a newly released survey from the National Association of REALTORS®. More than half of REALTORS® report their clients are taking on do-it-yourself home improvement projects in preparation, too.

“After a pause, home sellers are gearing up to list their properties with the reopening of the economy,” says Lawrence Yun, NAR’s chief economist. “Plenty of buyers also appear ready to take advantage of record-low mortgage rates and the stability that comes with these locked-in monthly payments into future years.”

NAR conducted an Economic Pulse Flash Survey May 3-4 and asked about 2,500 members how the coronavirus has been affecting their real estate business.

Home buyers are gradually re-emerging, but the pandemic has shifted some of their housing preferences, according to the results. Five percent of REALTORS® report that their clients have changed their neighborhood preferences from urban to suburban due to the pandemic. Also, one in eight REALTORS® surveyed say that buyers have changed at least one home feature that’s important to them since the COVID-19 pandemic. The most common features identified are home offices, yard space for exercising or growing food, and more space to accommodate their family.

But home buyers in search of a big bargain may not find one. Nearly 75% of REALTORS® report that their sellers have not reduced listing prices to attract buyers. Housing inventories are near record lows and that reduced competition may be prompting more sellers to stand firm on their home prices.