A Louisiana woman was arrested last week after a real estate professional reported to police that she was attempting to purchase a million-dollar home with fake income verification documents. Pamela Chandler, who was trying to buy the property in Benton, La., presented the agent with a document claiming she had access to a trust fund. But after researching the document, the agent believed the paperwork was fake and reported it to the Bossier Financial Crimes Task Force.

Police arrested Chandler on forgery charges; the task force alleges that Chandler altered a letter from an attorney to make it appear as though she had access to sufficient funds to purchase the home. Chandler faces two counts of forgery as well as outstanding warrants in Texas on unrelated charges of fraud and exploitation of children, elderly, or the disabled.

“Through the course of the investigation, task force members found that Chandler altered a letter from an attorney in an attempt to lead the REALTOR® to believe that she had access to sufficient funds to purchase the home,” city officials said in a statement. “The investigation also found that Chandler had used multiple aliases in the past, including the Goldwyn name. Taskforce members secured a warrant for Chandler’s arrest and worked with the REALTOR® to take her into custody.”

Chandler is being held at the Bossier Parish Jail.

At an open house, buyers will carefully size up a home, either to buy or simply out of curiosity. Here are a few details to pay particular attention to when prepping for an open house:

The front door: This is the first spot buyers see. Is the paint chipped? Are the lighting fixtures covered in spiderwebs? The front door could set the tone for the rest of the house on whether this is a well-kept house or one that lacks maintenance, Elizabeth Lucchesi, a real estate pro with the LizLuke Team with Long & Foster Real Estate in the Washington, D.C., area, told The Washington Post.

The smell: Every home has a scent, whether good or bad. Homeowners can become nose blind to the scent that their home is projecting. But new people coming in will notice.

Maintenance signs: Lucchesi suggests looking at the house carefully for any signs that show it hasn’t been properly maintained. For example, is there peeling paint on the trim outside? Is the house showing its age, such as with the appliances and countertops? Address any needed repairs or maintenance issues.

Plumbing: Visitors are undoubtedly going to open that cabinet under the sink. Is there any evidence of leaking under the sinks? Make sure the plumbing is up to par.

Windows: Are the windows foggy? If so, that’s a giveaway there’s a problem with the sealing. Lucchesi says make sure the windows open and close properly in an older home and that there are no other issues they present.

First impressions are everything, especially in home buying. A gorgeous exterior vs. a crummy one decides whether you walk in the front door. Inside, spotless interiors are more likely to inspire a life there than a cluttered house that’s clearly, well, someone else’s home.

And while this is where staging can play a huge role, it’s the listing pictures buyers see online that is often the first barrier of entry. So they better be really good.

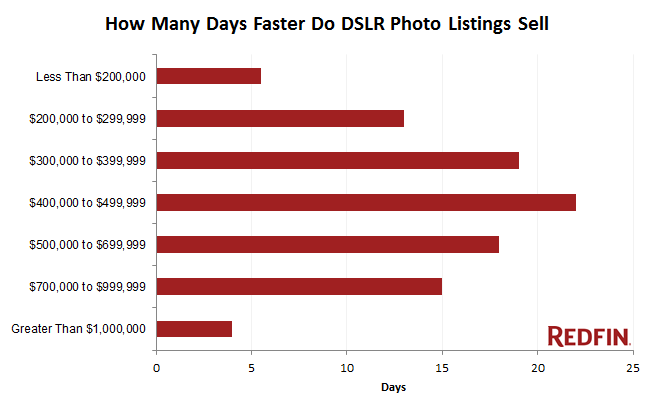

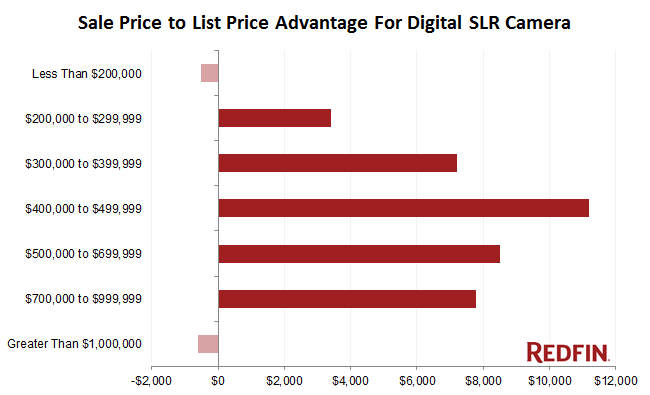

In fact, a 2013 Redfin study found that homes professionally photographed with high-performance Digital Single-Lens Reflex (DSLR) sold quicker and for thousands of dollars, more than homes shot with amateur photos. DSLR cameras are also the preferred camera of Redin’s national photography manager, Drew Larrigan. Redfin provides professional photography to all its listing clients, free of charge.

Why Professional Real Estate Photos Sell Homes for More

“The iPhone is the number one camera on the market right now, but we are still very far from it replacing a DSLR, which offers a higher quality image with higher pixelation. It’s the level necessary in this business, that will be continued to be used in the market for years to come.”

But you need more than just a fancy high-tech camera, you also need the know-how.

“The number one thing people get wrong with listing photography is having the mindset that anyone can do it and deliver a beautiful photo,” he said. “There is a lot of behind-the-scenes work you don’t see, capturing layers of High Dynamic Range (HDR) images to create one beautiful shot.”

Layers, he explained refers to multiple exposures. “This allows us to highlight shadows and bring out brightness or darkness through the windows. And then you stack those layers, which creates the beautiful windows in our photos.”

As online searching and browsing is a critical part of the home-buying process, it makes sense that professional photos will entice people to visit the home as they know what they are getting before they even set foot in the home.

“Today we have more shoppers buying from abroad or out of state and making an offer sight unseen, and really want to see a home documented,” Drew said. “They want to see every corner of the home, and that’s the beauty of the DSLR is offering a resolution that allows the out of state or city buyer a chance to see the home in full.”

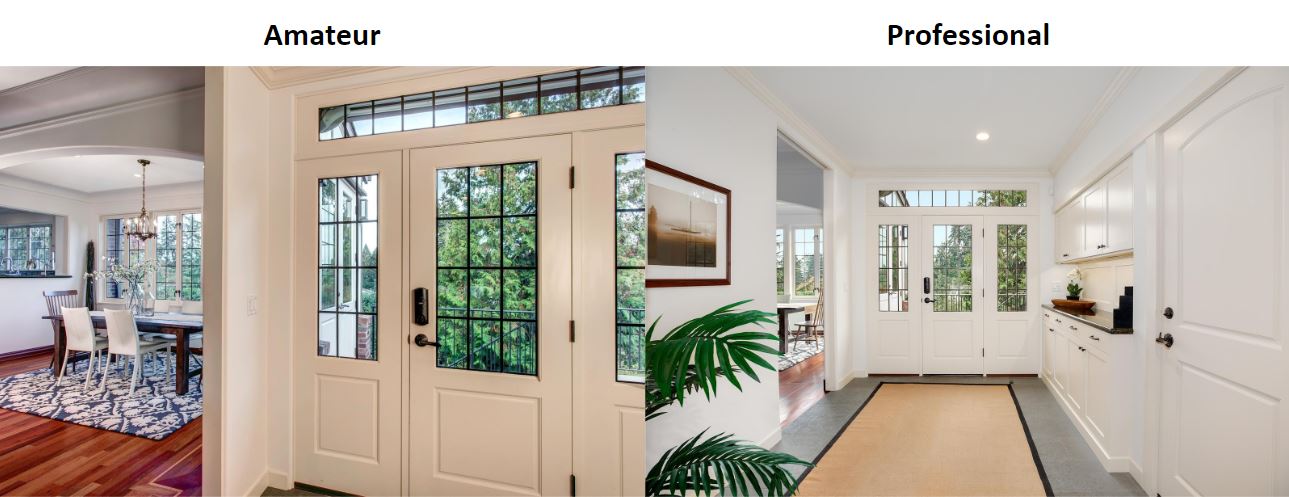

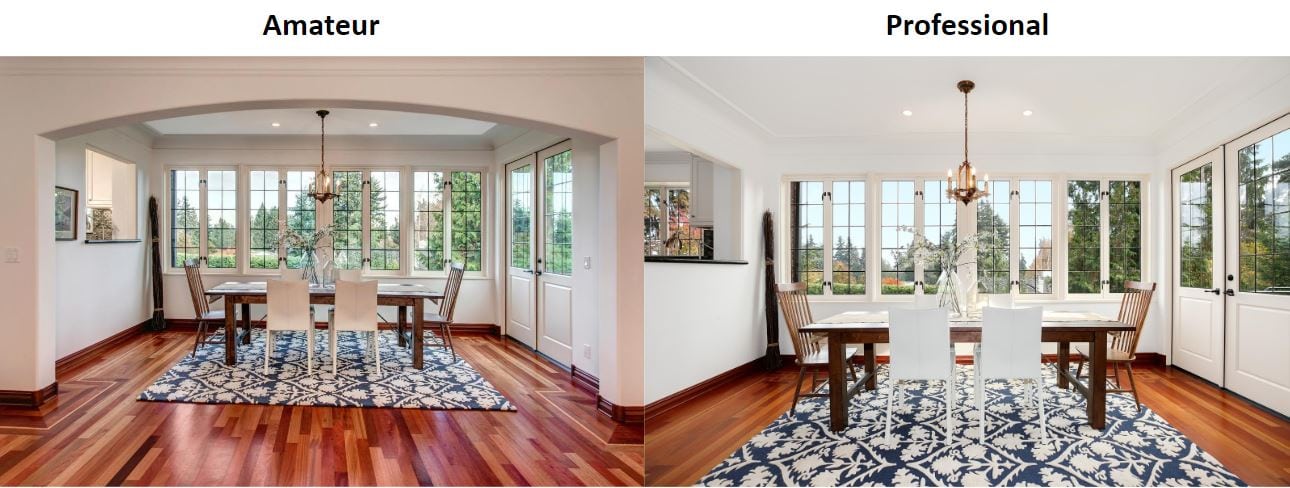

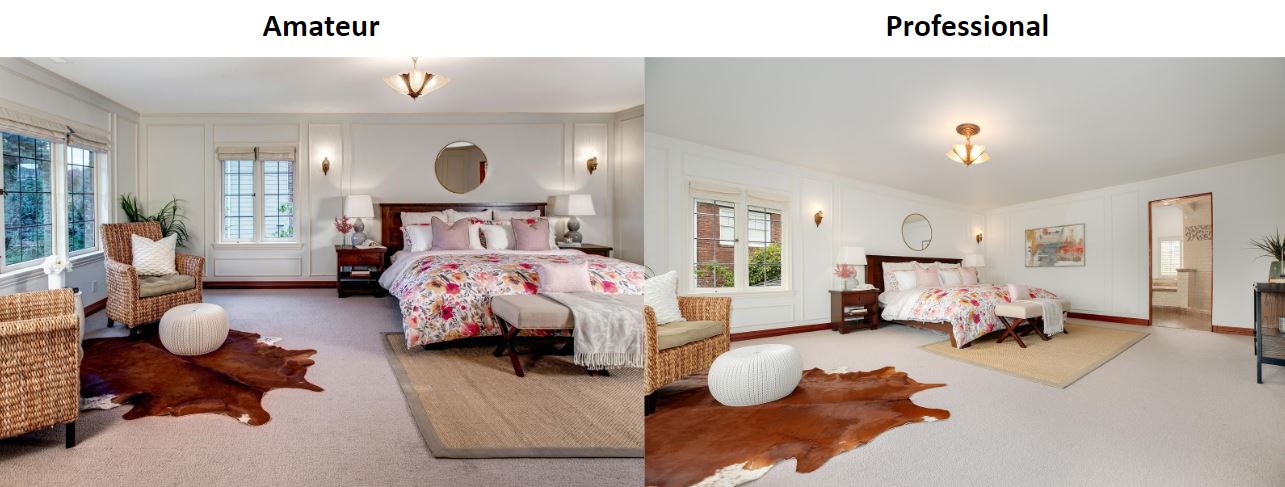

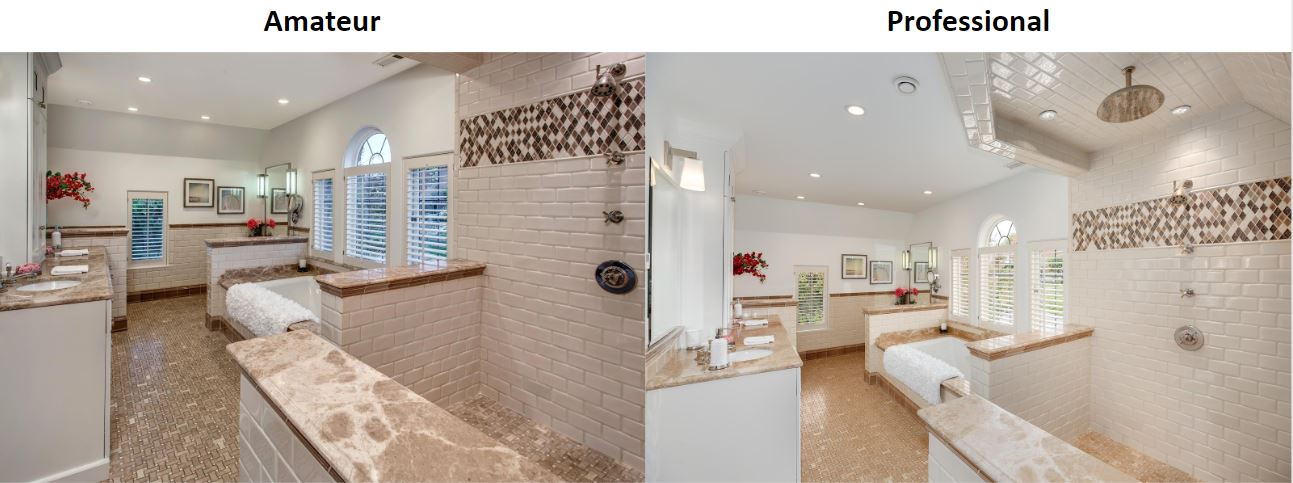

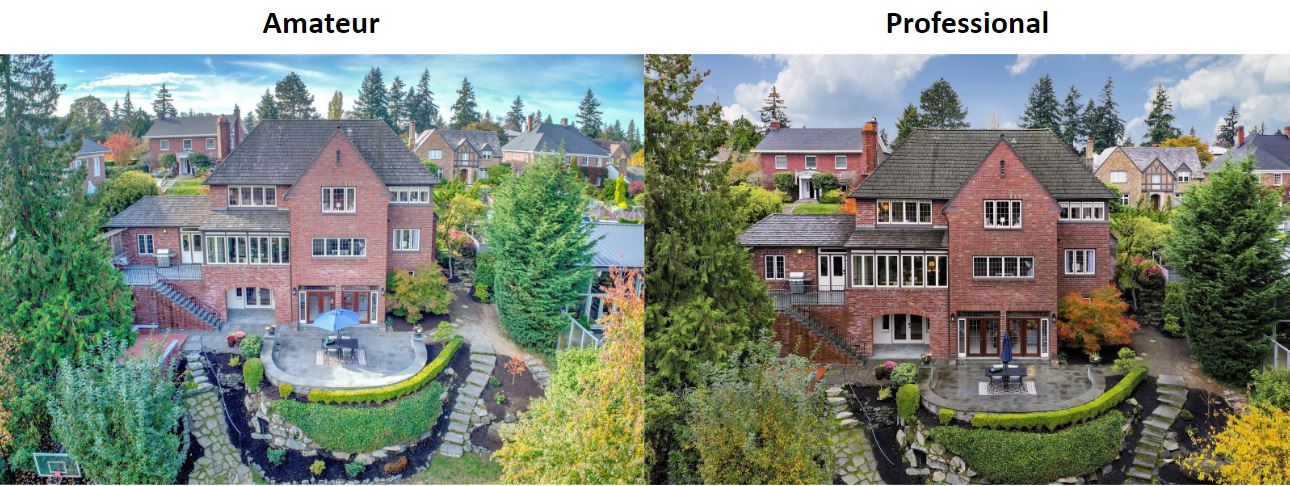

Amateur vs. Professional Real Estate Photos

To see these differences in action, Drew shared listing photos comparing those shot by an amateur, and those professionally photographed. “These examples are a chance to really look at the data visually, of the difference between a team approach that builds out quality, versus independent third parties,” he said. “It goes to show how important it is for Redfin to offer quality to the client, and how important it is to make sure our listings are as beautiful as possible.”

“In the above photo to the left, the photographer attempts to connect the front door with the dining area, but in the process, misses all the wonderful entry storage, and the white walls look brown. Redfin’s professional photo on the right chose to instead focus on the expansive hallway, beautiful entry, great storage, and crisp color tones. The professional photographer fully utilizes this space and frames key assets in the hallway.”

“In the professionally shot photo above on the right, the color tones, wood tones, and white balance are perfect. The walls are WHITE. The frame orientation is centered around the chandelier and the photo invites you into this room. In contrast, in the other photo, the room appears to be leaning, the white balance is off, and the colors are dark, almost reddish.”

“Once again, aproper color balance comes into play here. When incorrect, the master bedroom feels small. It also misses an opportunity to show the adjoining bathroom. The composition should highlight the full room to its entirety.”

“This bathroom is bright and light but the white balance is off, and as a result, the images miss key features like the upscale shower head, vanity and lighting.”

“In the first photo, your eye is drawn to other objects, rather than the house itself. The basketball hoop, open umbrella, neighbors to the left and right are distracting and more obvious. Additionally, the home isn’t centered, and the lens distortion bends the horizon line. When photographed correctly, you will notice the sky and the framing. This is a shot that is composed, center and square. The color tones are natural and the backyard feels private.”

Redfin Photos by: Matthew Deering

Homes professionally photographed with DSLR cameras are proven to sell quicker and for thousands of dollars more than homes shot with amateur photos.

Inspired by Drew’s insight, we took a look back at the 2013 study. The data revealed that professionally photographed homes priced in the $400,000 range sold three weeks faster and for more than $10,000 relative to their list price, than their counterparts with amateur photos.

Data 2013 study by Redfin

The 2013 findings also found that homes listed between $200,000 and $1 million sold for $3,400 to $11,200 more relative to their list prices when photographed professionally with a DSLR camera. At the high end of the spectrum, professionally photographed homes for more than $1 million sold at prices similar to those with amateur photographs.

Data based on 2013 Redfin study

Additionally, The 2013 findings also looked at photo sharpness, or, the detail added to a picture by using a good camera, lens and lighting. Whether a crisp reflection, or bright flowers, a sharper picture will show a house in its best light. The sharpest 10 percent of photos sold at or above list price 44 percent of the time, while listings with average sharpness sold at or above list just 13 percent of the time.

The kitchen is often considered the centerpiece of a home, so it’s not surprising that it tops most homeowners’ renovation lists. Homeowners are spending more to outfit their kitchens, too. Kitchen remodel spending jumped 27% in the past year, reaching a median of $14,000 on upgrades, according to a newly released Houzz & Home survey of more than 140,000 homeowners.

After the kitchen, the next biggest remodeling expenditures are for guest and master bathroom remodels, which increased over the past year by 17% and 14%, respectively, the survey found.

The higher overall costs on remodeling spending is likely due to the increased costs of imported building materials, the survey notes.

“Last year’s 10 percent increase in tariffs on imported building materials is likely one of several forces hitting consumer pockets in areas such as kitchen and bathroom remodels that are heavily dependent on imports of cabinetry, countertops, ceramic tile, plumbing fixtures, and vinyl flooring from China,” says Nino Sitchinava, Houzz principal economist. “We expect similar effects to take place in 2019 given the recent breakdown in trade negotiations.” (Also read Experts:Mexican Tariffs Would Hurt Housing Affordability.)

Slightly more than half of the 140,000 homeowners surveyed say they plan to continue or begin home renovations this year. They expect to spend a median of $10,000 on upcoming projects, the survey showed.

What are some of the most popular projects?

Security upgrades was one theme of projects that showed a significant rise in popularity. Homeowners are spending a median amount of $500 on items like smart outdoor security cameras, which can be monitored or controlled from a mobile device. Younger generations are the most likely to focus on home security upgrades, according to the survey.

Here’s a breakdown by theme of some other top decorating and remodeling projects.

The top home decor–related purchases among homeowners are:

·Pillows and throws: 51%

·Rugs: 50%

·Large furniture: 47%

·Artwork: 46%

·Small furniture: 44%

·Lamps: 39%

·Window treatments: 39%

·Storage/organization: 34%

·Mirrors: 28%

The top home improvement–related purchases among homeowners who renovated:

Young adults with low incomes or poor credit histories may ask their parents to co-sign on their mortgage—and it’s a growing trend. The share of co-signed mortgages rose nationwide from 13.7% in 2015 to 17.4% in 2018, according to ATTOM Data Solutions.

But there are risks to being a co-signer. “Whoever is co-signing has to bring substantial income because they have to be able to afford the new payments on top of all of their other debt,” Eric Boutcher, senior loan officer with Atlantic Coast Mortgage in Fairfax, Va., told The Washington Post. “You’re adding up both borrowers’ debt, and you’re adding up both borrowers’ incomes. It’s all-encompassing.”

Also, it’s the co-signers who are taking on the brunt of the risk because they are responsible for the payments if the person they’re co-signing for can’t afford them. “There’s no separation of who’s responsible for the debt,” Boutcher says. “They’re both equally responsible.” Therefore, the co-signer’s credit and their ability to borrow on their own can then be impacted if the borrower misses a payment.

For those willing to take on the risk, co-signing offers a path to homeownership for some. One lender recalls a recent example of a college senior who wanted to snag a low interest rate and buy a home prior to graduation, according to the Post. By getting his parents to co-sign on the loan, he was able to qualify for a mortgage. “He was able to buy the house before he started the job,” Alex Jaffe, branch sales manager at First Home Mortgage in Chevy Chase, Md., told the Post.

A great lawn adds instant curb appeal to a home’s first impression, but according to Reviewed.com, homeowners may be making one of these common mistakes in their lawn maintenance:

1. Cutting the grass too short. Most grasses should be cut no shorter than 2.5 inches, according to Reviewed.com. Anything shorter could impede the grasses’ ability to absorb enough sunlight to thrive.

2. Failing to water enough. Reviewed.com says that most grasses need 1 to 1.5 inches of water per week. “If you’re just turning on your sprinkler for 10 minutes a day, the water isn’t getting down to the grass’s deep roots, and a lot of that water is going to evaporate before the grass has a chance to absorb it,” the article notes. The grass needs about 30 minutes for most irrigation systems. Reviewed.com suggests a test: Place cans across the lawn and run the sprinkler for 30 minutes. Measure with a ruler the amount of water that collects in the cans. Adjust your timing, as needed, to get 1 inch per watering session. Another test: If you can see your footprints in the grass after you walk on it, that is a sign it’s time to water.

3. Watering at the wrong time of day. To minimize evaporation loss, water early in the morning before it gets too hot. Avoid watering at night, as cool water sitting on the grass overnight can increase disease, Reviewed.com notes. “Don’t rush out to water the grass the moment the sun comes out either,” the article notes. “Grass grows deeper roots when it gets slightly drought-stressed.”

4. Using too much fertilizer. If your grass turns brown, don’t just dump a bag of fertilizer on it. That can waste money and hurt your plants. You likely will need less fertilizer than you think. Follow the directions on the bag for how much to fertilize. Also, avoid applying powdered or granular fertilizer before a rain. It will run off with rainwater. Reviewed.com also notes that if you use compost, try three-fourths of a cubic yard per 1,000 square feet of lawn.

5. Applying fertilizer at the wrong time. Fertilizer will be the most beneficial for a yard in the spring and fall in most climates. “Fertilizer will help your lawn the most when it’s growing the most—that is, not in the middle of summer, when your grass gets stressed by heat and drought,” the article notes.

The number of homes selling at or above list price is on the decline, returning to historical norms, according to CoreLogic’s Home Price Index. That could be a relief to home shoppers whose budgets have been squeezed in recent years as home prices have soared.

The share of homes that sold at or above list price dropped to 31.1% in March—about the same level as in 2000 and 2001. That also represents a big change from a year ago. In the second quarter of 2018, the share of homes selling at or above list price peaked at more than 40% of total sales—nearly triple that of 2008. “As annual home price growth started to slow in the third quarter of 2018, the share of home buyers able to negotiate a better price began to rise,” CoreLogic researchers note.

But there is variation geographically. Sixty-nine percent of homes sold for at least the list price in San Francisco, which had the largest share of such homes, followed by Washington, D.C., at 50% and Minneapolis at 48%, according to CoreLogic. On the other hand, Chicago and Miami had the lowest share of homes that sold at or above the list price: 21% and 14%, respectively.

“Price pressures rapidly increase as supply drops below three months,” CoreLogic notes. In San Francisco, for example, the supply of homes for sale was at 2.3 months, and home buyers there paid an average 4.6% more than asking price. However, in markets like Miami, where the supply of homes was 10.9 months, home buyers had more negotiating power and saw average discounts of 7.8% in March.

Shopping around for a mortgage can provide savings beyond just the interest rate. Borrowers could save thousands in lender fees as well.

Borrowers who collect up to five offers from mortgage lenders could save more than $2,000 on mortgage fees, according to a new study from LendingTree of 300,000 loan offers. These extra fees include the costs for a mortgage application, underwriting, origination, appraisals, and up to 16 other fees that borrowers are charged by lenders.

Some mortgage fees are flat fees. Others may be based on a percentage of the loan amount.

“Most aspiring home buyers are focused on saving for their down payment—and they may not have budgeted for additional thousands of dollars in fees,” the study’s authors note.

About 7% of new-purchase borrowers paid no fees when taking out a mortgage, and 15% paid less than $500. On the other hand, 13% of purchase borrowers paid $5,000 in fees and 3% paid more than $10,000.

Taxes, flood certification, city and county stamps, and recording fees tend not to be negotiable. But other mortgage fees may be, researchers say.

“You can skip the back-and-forth by shopping around for the best rate and fees before you commit to a lender,” the researchers note. “In our study, we looked at the savings available to the same borrower who received offers from multiple lenders. The median spread between the highest and lowest fees proposed was $2,045 for people who received five offers or more. That’s a lot of money to potentially save.”

For the first time since January 2018, the 30-year fixed-rate mortgage has dropped below 4%.

“While economic data points to continued strength, financial sentiment is weakening with the spread between the 10-year and the 3-month Treasury bill narrowing as fears of the impact of the trade war with China grow,” says Sam Khater, Freddie Mac’s chief economist. “Lower rates should, however, give a boost to the housing market, which has been on the upswing with both existing- and new-home sales picking up recently.”

Freddie Mac reports the following national mortgage rate averages for the week ending May 30:

30-year fixed-rate mortgages: averaged 3.99%, with an average 0.5 point, dropping from last week’s 4.06% average. Last year at this time, 30-year rates averaged 4.56%.

15-year fixed-rate mortgages: averaged 3.46%, with an average 0.5 point, dropping from last week’s 3.51% average. A year ago, 15-year rates averaged 4.06%.

5-year hybrid adjustable-rate mortgages: averaged 3.60%, with an average 0.4 point, falling from last week’s 3.68% average. A year ago, 5-year ARMs averaged 3.80%.

In their search for affordability, home buyers are taking their house hunts further out from the city limits. Exurbs are the outskirts of major metro areas that lie beyond the suburbs. Many offer more land and greater affordability in new-home construction.

Single- and multifamily activity in the exurbs makes up only a small share of permit activity across the country, but their quarterly growth rates reached a new high in the first quarter of 2019, according to the National Association of Home Builders’ new Home Building Geography Index. Single-family permit activity has posted a 5.6% year-over-year growth rate, which is higher than that for large metro areas and suburbs, the index reveals.

“Being lower priced, housing in areas such as exurbs tend to be less sensitive to price changes and therefore were not as affected as suburbs of large metro areas by higher [mortgage] rates” last year, the researchers note. “As land is more freely available and cheaper in the exurbs than suburbs, building permit activity in this regional geography increased in an otherwise challenging quarter.”