The Federal Reserve issued an emergency rate cut on Tuesday amid growing fears over a U.S. outbreak of the COVID-19 disease. The 10-year Treasury note, which mortgage rates follow, plunged to a record low last week. Mortgage rates are already hovering at 2016 lows, but some financial experts say rates should be much lower.

Last week, Freddie Mac reported the 30-year fixed-rate mortgage averaged 3.45%, down from 4.35% a year earlier.

Mortgage rates are trending down, but they aren’t as low as the 10-year Treasury indicates, Bankrate reports. Factoring in 10-year Treasury rates, mortgage rates should be averaging around 3.2% or 3.1%, Lawrence Yun, chief economist for the National Association of REALTORS® told Bankrate.com.

“There are a few possible reasons rates aren’t lower,” Yun explains. “Lenders might think this is a good profit opportunity, assuming borrowers don’t care about a few basis points. Another reason would be for lenders to close the gates on customers as more people want to refinance and they don’t have the resources to manage an influx of new loans. And the third possible reason is the future of Fannie and Freddie’s government guarantee.”

Other financial experts also suggest the larger spread between the 10-year Treasury and mortgage rates is that lenders could be fearing that an outbreak of the disease could lead to a slowdown in the world economy or make mortgage-backed securities riskier (if more people then become late on paying their mortgage or default).

Nevertheless, “the fear gripping markets is driving bond yields sharply lower, with mortgage rates dropping, though not in lockstep,” says Greg McBride, Bankrate’s chief financial analyst. “Home buyers and those looking to refinance will find this an opportune time to lock in a rate at one of the lowest levels we’ve ever seen.”

When Connie Allen, 59, became single again, she was ready to leave the area of Tuttle, Okla., which she had called home since she was 8. Following the death of her parents and divorce from her second husband, she realized that caring for a 4,000-square-foot home and outbuildings on nearly seven acres was too much to keep up with alone. Moving roughly 20 miles to the town of Yukon would put her close to her daughters and grandchildren.

Connie Miller

Connie Allen, center, with the mother-son team of Connie and VJ Miller. Allen represents a trend: single women over 55 who are buying on their own.

While she was no stranger to real estate, Allen had never bought or sold a home without a partner. She turned to another Connie— Connie Miller, ABR, CRS, with the Miller Dream Team at Crossland Real Estate in Oklahoma City—to help her through the process.

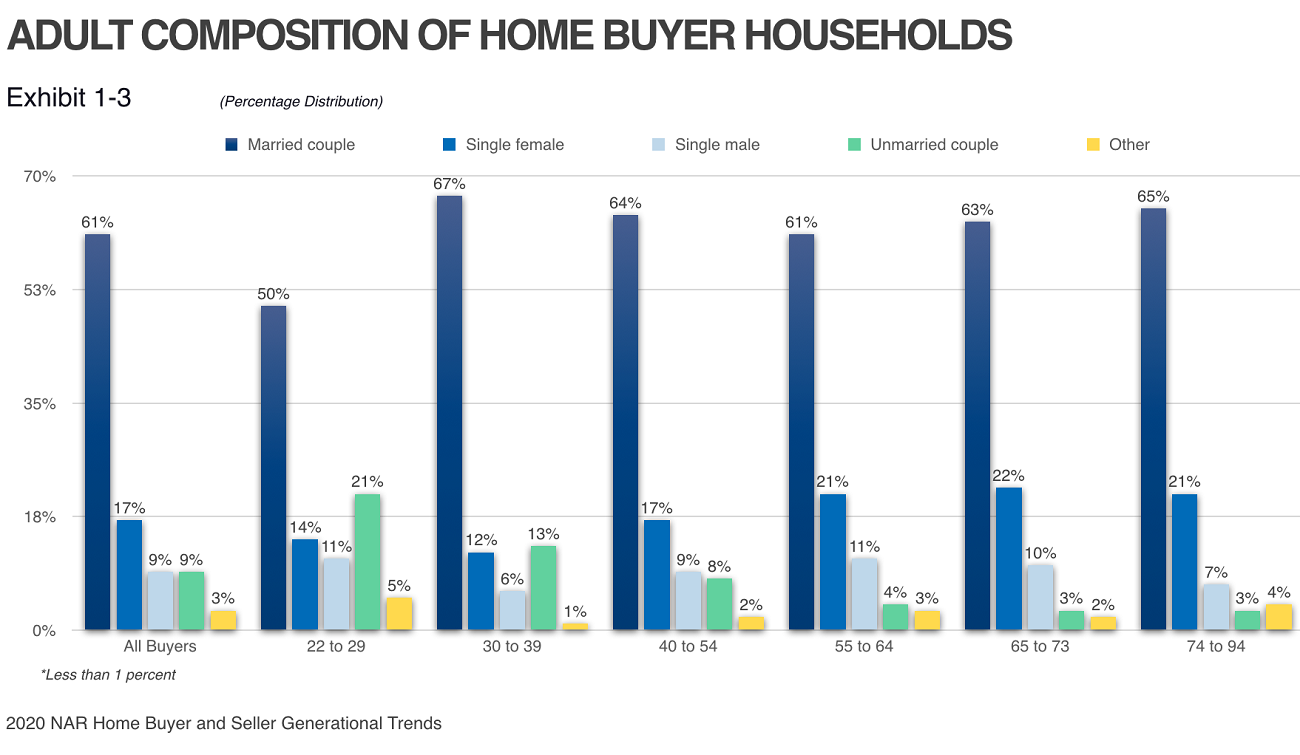

A new report from the National Association of REALTORS® shows that, in every age category, single women buy in higher numbers than single men. But much of the buzz about single-female buyers is often around young women delaying marriage and heading into homeownership on their own. It turns out older women may be a better customer target.

Married couples still make up the majority of buyers among all generations. But according to the 2020 Home Buyer and Seller Generational Trends Report, a significant 22% of the 65 to 73 years old home-buying population is made up of single women. Among 55- to 64-year-olds and 74- to 94-year-olds, 21% of buyers are single women. Compare that to younger generations, where the percentage of buyers who are single females ranges from 12% to 17%.

The takeaway: Real estate professionals may find success applying sales strategies for first-time buyers toward women who, like Allen, have been homeowners for many years but have never purchased on their own.

Behind the Data

Ali Whitley, ABR, CRS, a sales associate and director of education and training at RE/MAX Crossroads Properties in Akron, Ohio, says purchases by women over 55 are often tied to emotional life events, such as death or divorce. ”These can be very emotional transactions,” Whitley says. “They can be from the loss of a spouse and sometimes the loss of the financial breadwinner, too. They are trying to determine what to do next. There’s an emotional impact that may not have been there in any of their previous real estate transactions.”

“Graying divorce” also has increased, adding more mature singles to the housing market. Divorce rates among adults 50 and older have doubled since the 1990s and tripled among those 65 and older, according to data from the Pew Research Center. In 2018, 16.1% of people 55 and older were divorced—a record high—up from just 5% in 1980.

Working With Singles

Whitley says the single female buyer niche has grown enough that she highlights how to work with single women in the real estate course “Generational Buy,” which she teaches nationwide. “I encourage buyer’s agents to pay attention to this segment because they may require some additional empathy in a transaction and some additional time,” she says. “This may not be an exciting purchase for them, as is the case for buyers in other situations.”

Whitley recalls working with an older, single female client who had lost her spouse unexpectedly. “It’s not always the best time to make a big decision” after such a loss, Whitley says. “I needed to be cognizant that she needed to take time and make sure she wasn’t making a snap decision. Unless the transaction is motivated by a financial decision that will get the buyer into a better position — or it’s absolutely needed to move forward in life — a surviving spouse may be better off waiting for a year to make a decision with a clearer head.”

Even when a move isn’t motivated by the death of a spouse, purchasing alone is a big step. Your single client will likely take notice of the special attention you give her. “I appreciated Connie’s knowledge, warmth, and attention,” Allen says. “She checked on me all the time. She was very personable, very informative, but not pushy. She was more concerned about the person than the sale.”

Don’t Prejudge Their Preferences

Don’t make assumptions about the type of property single baby boomers are looking for; not all of them want to downsize to a smaller home. Certainly, some will be drawn to condo life, which relieves the financial and physical pressure of yard and exterior maintenance. But Whitley says she’s also had a large number of 65-and-over clients who desire a bigger home—three bedrooms or more—for their grandkids and family to visit. After all, being near family and friends is top of mind among older generations, NAR’s report shows. Among people 63 and older, the desire to be closer to friends and family was the top motivator for a home purchase.

That’s what motivated Allen’s move. When she toured her new home, she says, “I could picture the grandkids visiting here.” Allen also wanted a move-in-ready, modern home. Bonus: She’d cut her work commute dramatically.

Allen toured only two homes before making her decision, Miller recalls. Asked what special considerations she might make when selling to a less-decisive single woman, she said safety and home maintenance might be chief concerns. But there again, don’t prejudge. “Women are more independent today,” Miller says. “I see women now taking charge of having their own portfolio and doing their own work on their properties. It’s inspiring.”

The older, single female buyer cohort can be a rewarding business niche, Miller says. For one thing, there’s no concern about differing opinions between partners. Also, “I think older buyers tend to have more trust in us,” Miller says. “They like you to call them. They expect it. They don’t feel like they’re being treated properly if you don’t call. Younger buyers will wonder, ‘Why did you call when you could have texted?’”

Fewer homes were on the market in February compared to a year prior, and home prices are rising as inventory continues to tighten, according to realtor.com®’s February Housing Trends Report. That has prompted economists to predict a particularly competitive spring homebuying season.

National housing inventory dropped 15.3% year over year in February, the largest annual decline since realtor.com® began tracking inventory data. Twenty-five of the nation’s 50 largest metros saw their inventory decline by 20% or more. The largest inventory drops were recorded in Phoenix, San Diego, and San Jose, Calif., where decreases exceeded 36% year over year, realtor.com® reports. The inventory crunch pushed the median U.S. listing price up 3.9% to $310,000.

“The Fed’s decision to cut rates by 50 basis points earlier this week in reaction to concerns over the spread of COVID-19 [also called the coronavirus] is good for home buyers, but only if they can find a home to purchase,” says Danielle Hale, realtor.com®’s chief economist. “Finding a home remains the chief challenge in today’s inventory-starved market. Given the still-decreasing number of homes for sale in many markets, if a listed home is priced well, expect it to sell quickly this year. Construction of new homes will need to jump into overdrive in order to bring the nation’s supply and demand for housing back toward equilibrium.”

Further, Hale also says it remains unclear just how big of an impact the spread of the coronavirus could have on consumer spending, at least in the short term.

The latest housing numbers don’t take into account the mounting fears of COVID-19 outbreaks in the U.S. over the last week. However, last month, the housing market was robust. Home prices in 46 of the 50 largest markets in February were, on average, 6.5% higher than a year earlier. Philadelphia saw the largest home price increase in the nation, up 17% annually to $295,000.

The 30-year fixed-rate mortgage this week fell to its lowest average on record—3.29%—since Freddie Mac began tracking such data in 1971. And borrowers rushed to lock in.

Mortgage applications rose 10% last week compared to a year ago, says Sam Khater, Freddie Mac’s chief economist. “Given these strong indicators in rates and sales, as well as recent increases in new construction, it’s clear the housing market continues to be a positive force for the broader economy,” he adds.

Freddie Mac reports the following national averages with mortgage rates for the week ending March 5:

30-year fixed-rate mortgages:averaged 3.29%, with an average 0.7 point, falling from last week’s 3.45% average. Last year at this time, 30-year rates averaged 4.41%.

15-year fixed-rate mortgages:averaged 2.79%, with an average 0.7 point, falling from last week’s 2.95% average. A year ago, 15-year rates averaged 3.83%.

5-year hybrid adjustable-rate mortgages:averaged 3.18%, with an average 0.2 point, falling from last week’s 3.20% average. A year ago, 5-year ARMs averaged 3.87%.

Many home buyers are having a tough time finding a home they want, and the problem will likely get worse. A new study by Freddie Mac puts the housing shortage in a dire perspective: a 3.3 million unit deficit nationwide.

Years of underbuilding has created an inventory shortfall, which is most pronounced in states with strong economies that have been luring more people to move for jobs, Freddie Mac’s latest Insight report notes.

“Simply put, new housing supply is not keeping up with rising demand,” says Sam Khater, Freddie Mac’s chief economist. Freddie Mac’s report says the housing shortage is rising by about 300,000 units a year. “More than half of all states have a housing shortage, and the shortage is no longer concentrated in coastal markets but is spreading to the middle of the country, in more affordable states like Texas and Minnesota,” Khater adds.

Those interior states as well as others, such as Colorado, are now feeling the crunch and need to build more housing units to accommodate areas growing in population. “Domestic migration is worsening the housing shortage issue in some states,” the report notes. “In pursuit of new opportunities in states with stronger economies, people have migrated from states with surplus housing like West Virginia, Alabama, and North Dakota, to states with housing deficits, putting pressure on high-growth states.”

The Freddie Mac report estimates 29 states have a housing supply deficit, and the shortfalls are driving up home prices in areas where inventories are the tightest. The states with the highest deficits are Oregon, California, Minnesota, Florida, Colorado, and Texas.

“We are in the midst of a demographic tailwind, and we expect home purchase demand will remain strong well into the next decade as the peak cohorts of millennials turn thirty years of age in 2020 and beyond,” Khater says. Freddie Mac predicts the housing shortages to worsen, too, as millennials and Generation Z enter the housing markets to form their own households over this decade. That will prompt home prices to continue to rise, the report notes.

On Tuesday, the Federal Reserve announced its first emergency rate cut since the financial crisis due to mounting concerns over the economic impact from a potential coronavirus outbreak in the U.S.

The Fed’s rate cut was unscheduled. It also marks the largest one-time cut—half a percentage point—since 2008.

The Federal Reserve’s funds rate—what banks charge one another for short-term borrowing—isn’t directly tied to mortgage rates, but it can influence them. Long-term fixed mortgage rates are usually more tied to the yield on U.S. Treasury notes.

“The coronavirus has quickly upended globe economic expansion and introduced the significant uncertainty of a possible recession,” says Lawrence Yun, chief economist at the National Association of REALTORS®. “Today’s interest rate cut is therefore an appropriate response to changing events. The real estate sector will hold up very well because of the rate cut. Hesitant home buyers will be enticed to take advantage of low interest rates. Commercial property prices will rise due to higher returns that can be had from the bond market after adjusting for risks.”

Mortgage rates have already fallen since the beginning of this year and are now hovering at the lowest averages since 2016. Freddie Mac reported last Thursday that the 30-year fixed-rate mortgage averaged 3.45%, down from 4.35% a year earlier.

Continued downward movement in the 10-year Treasury market could press mortgage rates lower, Rick Sharga, president and CEO of CJ Patrick Company, a financial services consulting firm, told MarketWatch. “I wouldn’t be surprised to see 30-year loans with 3.0% rates before things settle back down,” Sharga says.

As for the Fed’s new benchmark interest rate, it’s now at a range between 1% and 1.25%.

“We saw the risk to the outlook to the economy and chose to act,” Fed Chairman Jerome Powell said at a press conference on Tuesday. He added that he expects the U.S. to fully recover after the coronavirus outbreak and fears subside. “I don’t think anybody knows how long it will be” until the potential economic fallout from the virus rebounds, Powell said. “I know the U.S. economy is strong and we’ll get to the other side of this and return to solid growth and a solid labor market as well,” he added.

Until then, Powell did leave the door open to further rate cuts, if necessary. “It’s possible you’ll see more individual action—more action moving forward,” he said.

The rapid international spread of the coronavirus is striking fear in investors and shaking financial markets. With 89 confirmed cases in the U.S. as of Monday morning, how could the near-pandemic impact the housing market? So far, coronavirus fears have prompted mortgage rates to drop. Investors are pulling their money out of stocks and putting it into steadier U.S. Treasury bonds—and when bonds perform strongly, mortgage rates tend to dip, realtor.com® reports.

But while the coronavirus may have the effect of dampening home sales in some segments of the market, low mortgage rates will continue to entice buyers and sellers, National Association of REALTORS® Chief Economist Lawrence Yun says. “Mortgage rates likely will fall to an all-time low, and buyers will want to lock in, even with growing economic concerns,” Yun says. “But expect far fewer international buyers because of travel concerns.”

Still, the freefall in the stock market is a worrisome sign. “People don’t make big decisions in a vacuum, and buying a home is a big one,” says Danielle Hale, realtor.com®’s chief economist. “If the stock market is flashing a sign that an economic slowdown is on the way, that’s when Main Street will feel it. And it could lead to a slowdown in home sales.”

The luxury housing market could be the most vulnerable, housing analysts say. Wealthy buyers tend to have more money invested in stocks. And “if you’re feeling less wealthy, you’re less likely to make a large purchase,” Hale says.

Further, Chinese buyers, whom have comprised the largest segment of foreign purchases in the U.S. over the last few years, are purchasing fewer properties, according to the National Association of REALTORS®. A temporary travel ban has been in place in order to prevent the spread of the virus, and that likely will lead to a big dip in purchases from foreign buyers.

Nevertheless, low mortgage rates may entice some buyers to purchase now rather than wait. NAR reported last week that contract signings climbed 5.2% in January compared to the previous month and were up 5.7% from a year ago. The 30-year fixed-rate mortgage fell to 3.45% last Thursday, Freddie Mac reported. “Buyers right now are trying to juggle whether or not they should jump in when mortgage rates are this low,” Ali Wolf, director of economic research at Meyers Research, told realtor.com®. “What looks like a home that’s out of reach may actually be very affordable on a monthly payment schedule.”

Low mortgage rates could cause a boost in home sales in the short term, Hale adds, but it depends on how much the virus continues to spread in the U.S. “At the very least, the coronavirus could cause some people to put home sales on hold,” says Hale. Globally, there have been 88,443 confirmed cases of the coronavirus, which causes flu-like symptoms. There have been 3,041 fatalities from the virus, 2,912 of which have been in China, according to data from the Centers for Disease Control and Prevention.

Some items in older homes should not be touched in a remodel, designers warn.

Homeowners should hold off on removing certain architectural details because they could be removing some selling points in the process.

“Architectural features that give homes distinct character should be left intact,” Patrick Garrett, a broker and owner at H&H Realty in Trussville, Ala., told realtor.com®. “There are home buyers looking for homes with unique features and older homes with character and charm.”

Realtor.com® highlighted several qualities in older homes that shouldn’t be touched, and molding was at the top of the list.

“On the inside of the home, the first things we salvage are the staircase, window trim, and crown molding,” Thomas Kenny, co-founder of Scott Simpson Design + Build in Northbrook, Ill., told realtor.com®. “The original molding, in particular, gives the home character and is usually crafted from high-quality materials that will stand the test of time.”

Stained glass is another feature that experts recommend keeping, and it can make a home more valuable. “Once you come across [stained-glass windows], you will remember them for a lifetime,” Anastasios Gliatis, CEO at Anastasios Interiors in New York City, told realtor.com®. “They also provide a spiritual, peaceful feeling, since they are identified with churches.”

Exposed brick walls are nothing to put a sledgehammer too either. Instead, make it the focal point of the room, says Laurie DiGiacomo, principal designer at Laurie DiGiacomo Interiors in Ho-Ho-Kus, N.J. “You should not remove exposed brick, because it lends a unique architectural element that brings texture and a rustic vibe to a space,” she told realtor.com®.

Don’t touch those doors either, designers add. Solid core and paneled doors don’t compare to todays’ big-box styles. “Old solid-core doors, and often their metal elements like doorplates, are real gems,” Jonathan Self, a real estate professional at Center Coast Realty in Chicago, told realtor.com®. “You can’t buy these with any amount of money, because the craftsmanship it takes to make them doesn’t exist anymore.” Gliatis adds that preserving paneled doors that include brass knobs and hinges is particularly a smart move because they are expensive and difficult to find nowadays.

Real estate pros are having a busy winter, and with buyer demand high, it could be even busier if it wasn’t for a lack of inventory continuing to plague many markets. Pending home sales rebounded in January, rising 5.2% month over month, the National Association of REALTORS® reported Thursday. Contract signings are up 5.7% over year-ago levels.

“This month’s solid activity—the second-highest monthly figure in over two years—is due to the good economic backdrop and exceptionally low mortgage rates,” says Lawrence Yun, NAR’s chief economist. “We are still lacking in inventory. Inventory availability will be the key to consistent future gains.”

The higher sales numbers are emerging despite combined inventory levels in December and January falling to the lowest levels since 1999, NAR reports.

NAR’s Pending Home Sales Index is a forward-looking indicator based on contract signings. Contract signings in January were up month over month in every region of the U.S., except the West, which saw a minor drop in activity. Sales, however, posted annual gains in every region of the U.S.

Lack of housing inventory continues to weigh on the housing market. But that hasn’t chipped away at buyer demand, even in the colder months when business typically slows.

“With housing starts hovering at 1.6 million in December and January, along with the favorable mortgage rates, among other factors, 2020 has so far presented a very positive sales climate,” Yun says. “Moreover, the latest stock market correction could provide exceptional, even lower mortgage rates for a few weeks, and that would help bring about a noticeable upturn in the coming months.”

Borrowing costs continue to head lower, enticing home shoppers and refinancers to lock-in.

“Given the recent volatility of the ten-year Treasury yield, it’s not surprising that mortgage rates again have dropped,” says Sam Khater, Freddie Mac’s chief economist. “These low rates combined with high consumer confidence continue to drive home sales upward, a trend that is likely to endure as we enter spring.”

Freddie Mac reported the following national averages with mortgage rates for the week ending Feb. 27:

30-year fixed-rate mortgages: averaged 3.45%, with an average 0.7 point, falling from last week’s 3.49% average. Last year at this time, 30-year rates averaged 4.35%.

15-year fixed-rate mortgages: averaged 2.95%, with an average 0.8 point, falling from last week’s 2.99% average. A year ago, 15-year rates averaged 3.77%.

5-year hybrid adjustable-rate mortgages: averaged 3.20%, with an average 0.2 point, falling from last week’s 3.25% average. A year ago, 5-year ARMs averaged 3.84%.

Mortgage rates fluctuate, and over the last 50 years they’ve changed significantly, Freddie Mac notes in a recent blog post. Consider, in the 1970s, the average rate was 8.86% compared to today’s 3.45%. Freddie Mac compiled the following chart to show how much mortgage rates have changed over the last five decades.